Firm Mobility, Attest among Top Profession Trends in State Legislatures

March 27, 2017

With 2017 legislative sessions well underway, states are seeing multiple legislative trends impacting the CPA profession, including full CPA firm mobility, the comprehensive definition of attest, taxation of professional services and human resource issues.

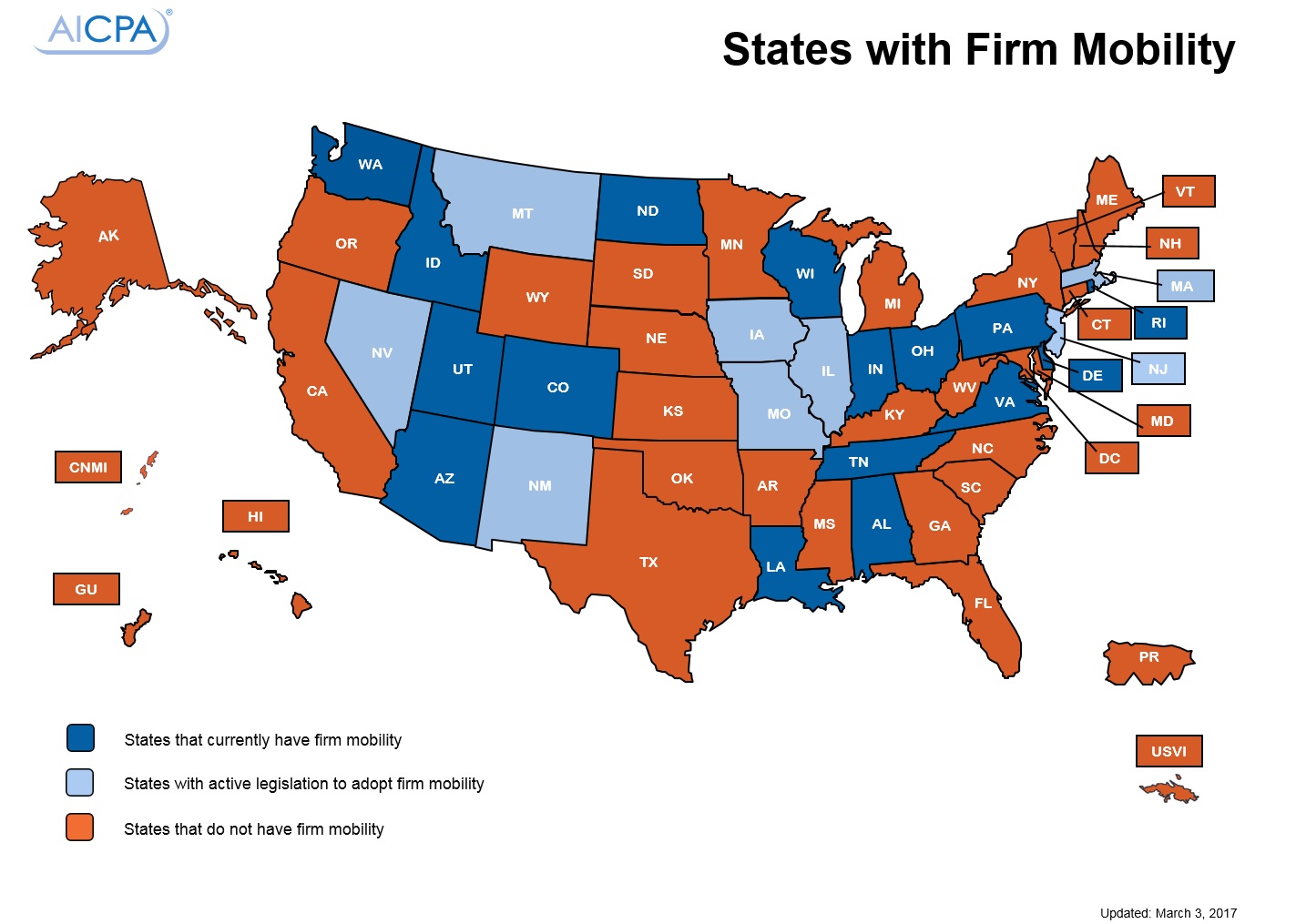

CPA Firm Mobility

Eight states – Iowa, Illinois, Massachusetts, Missouri, Montana, Nevada, New Jersey, and New Mexico – have introduced legislation to allow CPA firms from outside the state to perform attest services without registering their firms in the state. New Mexico’s bill recently passed the legislature and is pending the Governor’s signature. Montana and Iowa’s bills passed the first house.

Currently, 16 states provide for full CPA firm mobility. CPA firm mobility gives the public more choices in services provided by CPA firms, while maintaining public protection. CPA firms are subject to the laws and rules of every state in which they practice, and state boards of accountancy have the authority to investigate, fine, or otherwise punish all CPAs practicing in their state.

The AICPA and the National Association of State Boards of Accountancy (NASBA) included CPA firm mobility in the seventh edition of their model state act, the Uniform Accountancy Act, in May 2014. The provision is an extension of the popular individual mobility initiative that allows individual CPAs to provide non-attest services without having to obtain a reciprocal license.

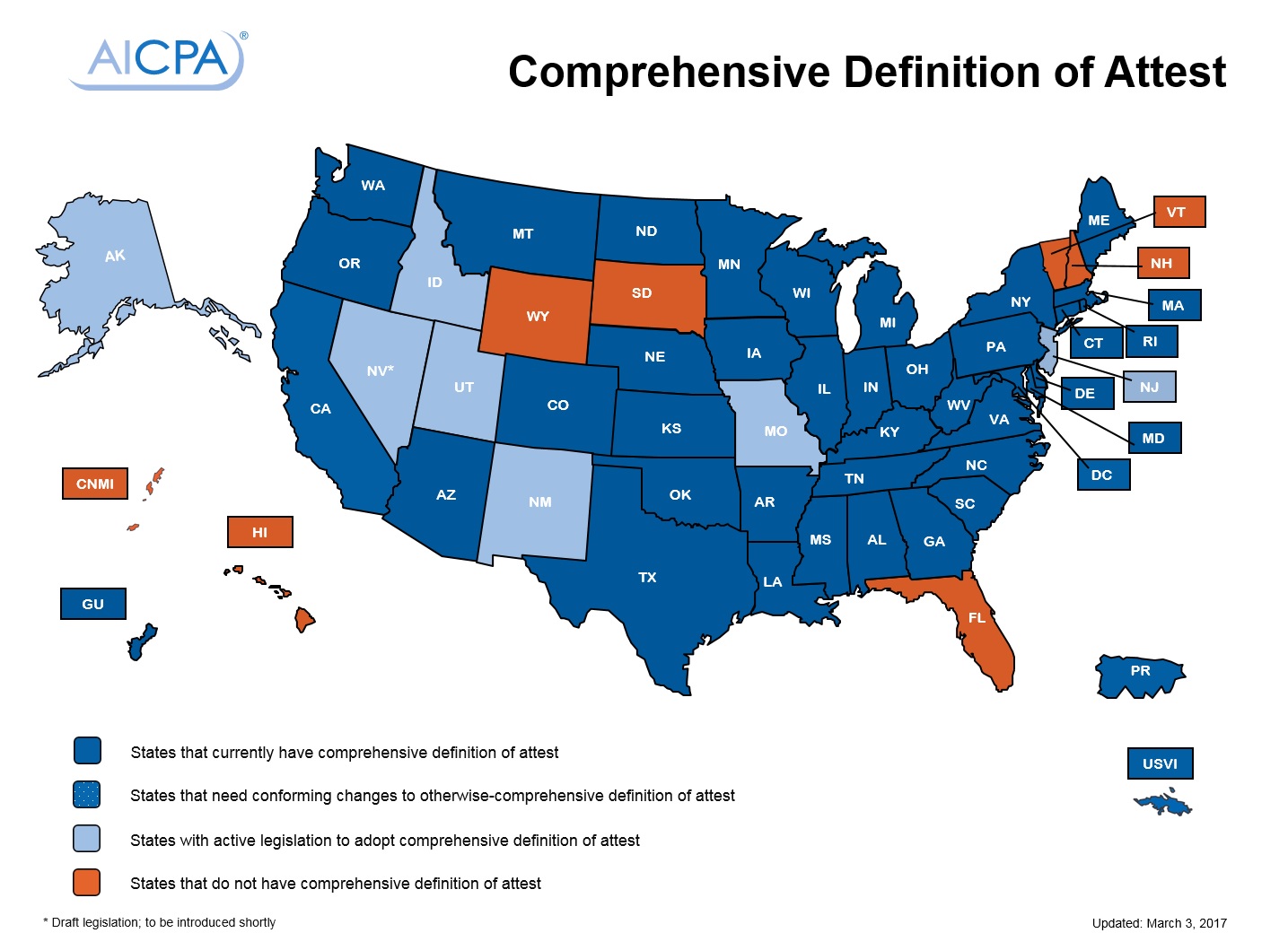

Comprehensive Definition of Attest

Arkansas and the District of Columbia recently became the first states in 2017 to adopt the comprehensive definition of attest. In total, 41 states now have the comprehensive definition in their laws.

Additionally, six other states – Alaska, Idaho, Missouri, New Jersey, New Mexico, and Utah – have pending legislation. New Mexico and Utah’s bills recently passed the legislature and are pending their respective governors’ signatures. Idaho’s bill passed the first house.

The demand for attest services has changed significantly, expanding to engagements such as security and privacy controls and sustainability. In states without the comprehensive definition, other marketplace participants can offer these services while using the CPA profession’s standards, but without the same credentials, experience, or regulation. Adopting the comprehensive definition of attest ensures that only CPAs operating in a CPA firm can provide attest services under the profession’s standards.

Taxation of Professional Services

Several states have introduced legislation to impose taxes on professional services. Some states, such as Indiana, are creating interim study committees to examine expanding the sales tax base. Others, such as Nebraska and Utah, introduced bills to directly tax professional services, including tax preparation and payroll services. So far, twelve states – California, Georgia, Indiana, Kansas, Kentucky, Missouri, Nebraska, Oklahoma, South Dakota, Utah, West Virginia, and Wyoming – have introduced tax on professional services legislation. The profession, including state CPA societies, is working against such measures.

Human Resources

Thus far in 2017, 40 states have introduced legislation related to human resources, including expungement of financial crimes from criminal records, pay equity, universal paid leave and pre-employment inquiries such as ban the box. The District of Columbia, Hawaii, Missouri and Oklahoma introduced legislation to mandate paid leave for employees administered through a government run fund. Several states, such as California, Idaho, Maryland, Oklahoma and Washington, also have pending legislation prohibiting employers from inquiring into a job applicant’s salary history. The AICPA is working with state CPA societies to seek exemptions for the CPA profession from such measures as appropriate.

For more information on these and other measures, visit the AICPA State Regulation and Legislation webpage or email state@aicpa.org.

{kind=link}

{kind=link}